Morning Comment: Several Overseas Markets Showing Some Cracks.

The Treasury market rallied very nicely yesterday, and this obviously led to a rather material drop in long-term interest rates. However, instead of that causing a nice bounce in the stock market, stocks got hit quite hard. In our minds, it looks like the stock market is finally beginning to wake up to the fact that the odds are now low that the economy will re-open as quickly as the vast majority of pundits on Wall Street have been calling for over the past several months.

No, this does not mean that we’ll see any kind of renewed MAJOR lock-downs (like we saw last year), but since the stock market is priced for perfection, any kind of delay in the re-opening…especially if it includes the resumption of some old restrictions in the U.S.…could/should create some material selling pressure in the U.S. stock market.

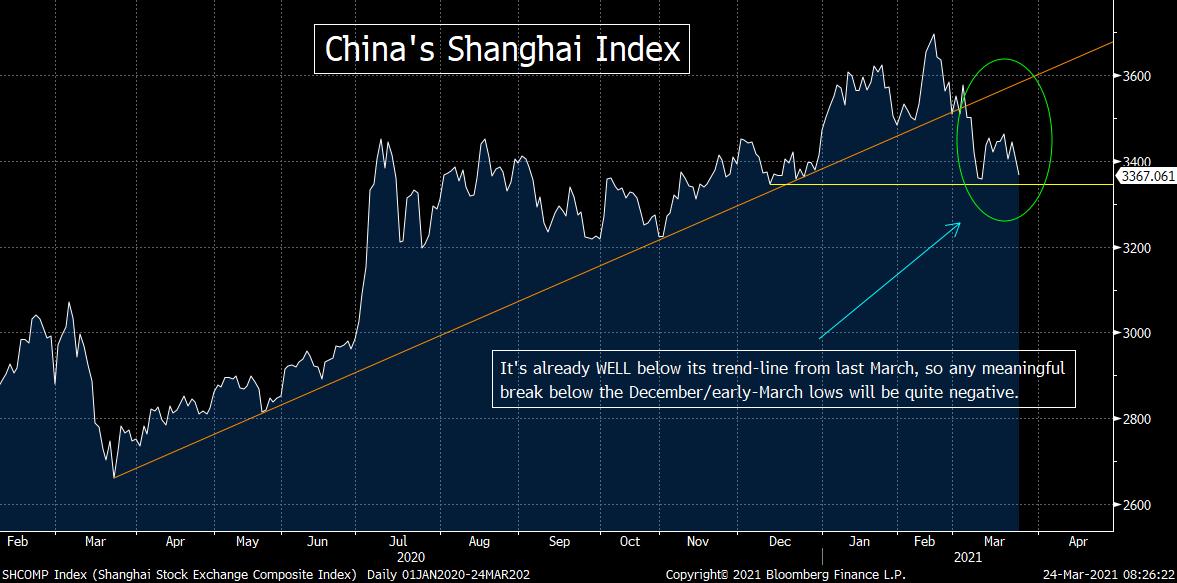

As for other stock markets around the world, some of them are already seeing some noticeable weakness. We highlighted the weakness in China’s Shanghai Index last week…and it has fallen further this week. China’s stock market has fallen almost 9% over the past month. This has taken the Shanghai Index well below its trend-line from the March 2020 lows and it is now very close to testing an important support level. The 3,345 level (just 0.5% below where it closed last night) is where the 200 day moving average comes-in. That level was ALSO the lows from both December and earlier this month…so any further weakness would also give it a key “lower-low”……Therefore, any meaningful break below 3,345 should signal that more weakness is very likely coming in China’s stock market.

We’d also note that Japan’s Nikkei index has seen some visible weakness lately. This weakness has been more recent…and hasn’t been as strong as it has been in China. However, the Nikkei is still down 6%...and it has broken below its trend-line from early November…AND made a slight “lower-low” below its mid-March lows.

Again, this is not as concerning as the move in China’s stock market. The “lower-low” is only a very slight one so far…and although the Nikkei has broken below its trend-line from November, it still remains 4%-5% above its more important trend-line from last year’s March lows. However, it still tells us that we’re beginning to see some cracks in this key overseas market as well.

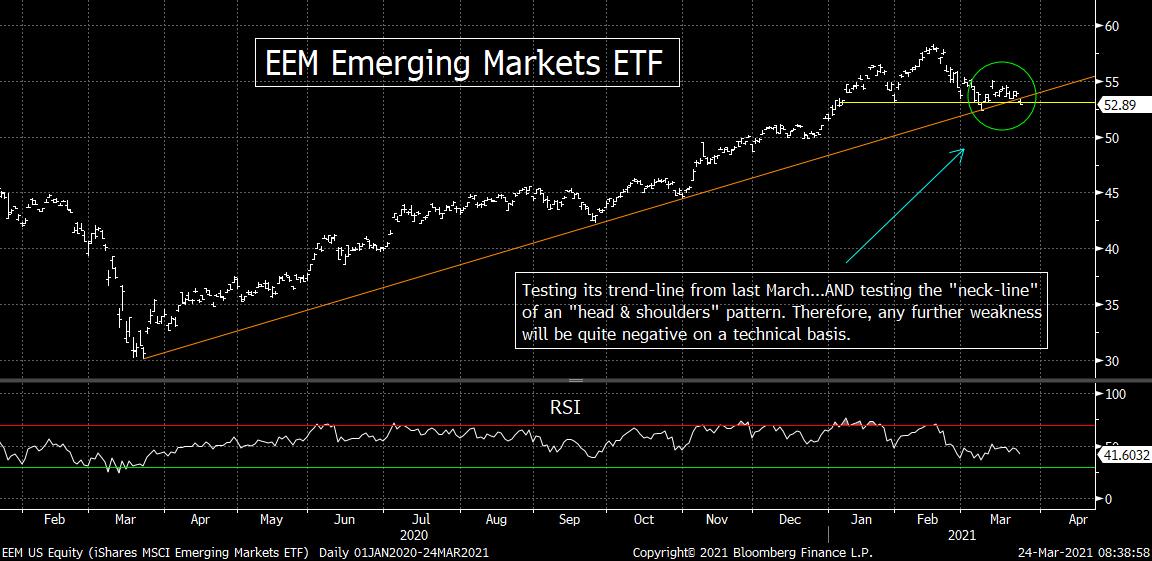

Finally, we’re also seeing the EEM emerging markets ETF testing a key support level. The 8.7% decline in the EEM over the last months now has it testing its trend-line from March of last year. More importantly, however, it is ALSO testing the “neck-line” of an “head & shoulders” pattern in-and-around the $52.50 level. Thus any further drop in the EEM will be quite negative for this asset class on a technical basis as well.

Our concern for the EEM is particularly high…because the DXY dollar index is moving in the other direction…and is now testing its highs from earlier this month. If the DXY breaks above 92.50 in any meaningful way, it will take it above its 200 DMA for the first time since last May…AND give it its second “higher-low/higher-high” sequence this year! Since the DXY dollar index has already broke WELL ABOVE its trend-line from March 2020, this would be a VERY compelling indication that the intermediate-term trend in the greenback is indeed changing this year…much like we have been saying it would for many weeks.

If, repeat IF, we do get confirmation that the rise in the dollar is something that’s going to last for a while (EVEN though it is likely to resume its decline later this year), it will be a clear indication that the recent underperformance of the emerging market will continue going forward. (It will also indicate that it is very likely that the pull-back in commodities we’ve been calling for will also continue for longer than most people have been expecting.)

In other words, the cracks we’re seeing in the U.S. stock market…with the recent weakness in the Nasdaq and the Russell 2000…is not isolated to the U.S. stock market. We are seeing cracks in several other key stock markets around the globe…and it gives us more confidence that the correction in the stock market we’ve been calling for recently will indeed come to fruition.

Matthew J. Maley

Chief Market Strategist

Miller Tabak + Co., LLC

Founder, The Maley Report

TheMaleyReport.com

275 Grove St. Suite 2-400

Newton, MA 02466

617-663-5381

Although the information contained in this report (not including disclosures contained herein) has been obtained from sources we believe to be reliable, the accuracy and completeness of such information and the opinions expressed herein cannot be guaranteed. This report is for informational purposes only and under no circumstances is it to be construed as an offer to sell, or a solicitation to buy, any security. Any recommendation contained in this report may not be appropriate for all investors. Trading options is not suitable for all investors and may involve risk of loss. Additional information is available upon request or by contacting us at Miller Tabak + Co., LLC, 200 Park Ave. Suite 1700, New York, NY 10166.

Recent free content from Matt Maley

-

THE WEEKLY TOP 10

— 10/23/22

THE WEEKLY TOP 10

— 10/23/22

-

Morning Comment: Can the Treasury market actually give the stock market some relief soon?

— 10/21/22

-

What Do 2022 and 1987 Have in Common?

— 10/19/22

-

Morning Comment: Which is it? Is stimulus bullish or bearish for the stock market?

— 10/17/22

-

Morning Comment: Peak Inflation is Becoming a Process Instead of a Turning Point

— 10/13/22

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464