Morning Comment: Great Potential Opportunities in Energy & Bank Stocks

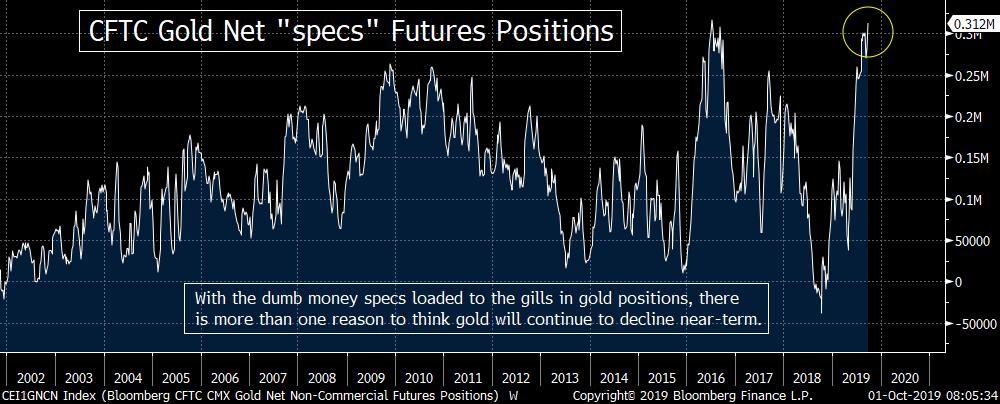

- Broken “neck-line” and “positioning” issues mean gold should see more downside movement near-term.

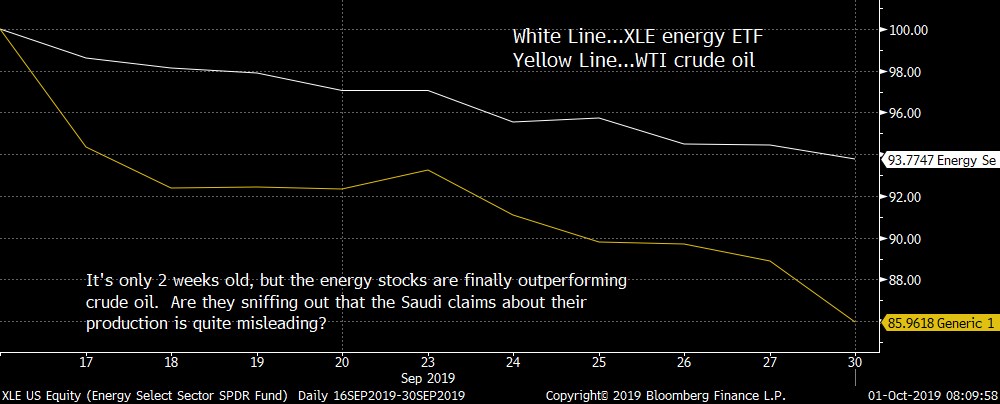

- Energy stocks are suddenly outperforming crude oil…and Saudi production claims misleading.

- BOJ shifting bond purchases. That’s good for the yield curve…and thus bullish for the bank stocks.

- Earnings season should provide headwinds, but group rotation should still provide nice opportunities.

Nice day yesterday, but it’s hard to draw any compelling conclusions from the action.

The last day of the third quarter gave us a nice little pop in the stock market, but it came on low volume and breadth that was mediocre at best. (The advancers vs. decliners was just 2.3 to 1 positive for the S&P 500 and only 1.3 to 1 positive for the NYSE Composite index. Even the Nasdaq…which rallied 0.75%...had breadth that was almost flat at just 1.1 to 1 positive.)…..As we said yesterday morning, it would be hard to make any conclusions from Monday’s action…and that certainly turned out to be the case.

Dollar up, gold down. Gold breaks key short-term support and long positions are extreme.

The DXY dollar index broke out it’s highest levels since the most recent dollar rally began in early 2018…and now stands at it highest levels since May of 2017…..It’s hard to say that the sharp advance in the dollar had a negative impact on gold yesterday…because the yellow metal spent the entire summer ignoring the rising dollar to rally more than 20%. However, there’s no question that gold got hit hard yesterday…falling over $20. This decline took gold below its September lows…and below the “neck-line” of a “head & shoulders” pattern.

In other words the sharp decline in gold probably had a lot more to do with the fact that it broke a key short-term support level than anything that had to do with the dollar. However, if you look at the most recent COT data, it shows that the dumb money “specs” are loaded to the gills in gold. So when you combine the broken “neck-line” with the “positioning” situation…and there seems to be a good chance that we’ll see more downside movement in the yellow metal before it stabilizes in a material way.

Having said this, we are still bullish on gold over the longer-term. It remains WELL above its eight year trend-line AND its critically important breakout level of $1,380 (the highs from 2016, 2017 and 2018). In fact, it might not have to fall by a huge amount. The $1,450 level was the “old resistance” level, so that should now offer some support over the coming days. Below that level, we have the early August lows of $1,400. If gold were to fall THAT far (which is a BIG “if”), we’d back up the truck.

Energy stocks finally outperforming WTI…that’s bullish. Also, Saudi production claims are very misleading.

Another commodity that got hit yesterday was crude oil…as WTI fell almost 3%. However, despite this decline, there are reasons to think that the energy equities could still be a great group for the 4th quarter. Since crude oil topped-out right after the attacks on the Saudi oil facilities, the energy stocks have actually (and finally) outperformed the price of crude oil. Since that September 16 spike in crude, WTI has fallen 13%...while the XLE has “only” declined 6%. Similarly, WTI has retraced more 75% of its rally off the August lows…while the XLE has retraced 50%.

This outperformance is only two weeks old, so it’s hard to get too excited about this development yet. However, the rhetoric surrounding the Saudis restoring their oil production sooner than expected is a very, very misleading. The problem with these claims by the Saudis is that their definition of production includes annual production plus sales from inventory. They haven’t fixed these damaged facilities, that’s going to take months. They’re using increased production from other facilities AND the above-mentioned inventories.

Some reports show that more than 1/3 of the “back to normal production” is coming from existing inventories. They cannot tap those forever…and like we said, it’s going to take many months to repair the damaged facilities. So the stories that things will be back to normal soon are a farce…and thus the odds that we’ll get another pop in crude oil due to supply concerns are higher than most people think (whether there’s another attack or not). We wonder is this is something that the energy stocks are pricing-in with their recent out-performance.

BOJ shifts gears…as global central banks shift their goal towards steeper yield curves. That’s bullish for banks.

Finally, as we mentioned on Bloomberg Radio early this morning, we thought the poor performance of the 10yr bond auction in Japan last night was quite telling. The BOJ has said they will potentially slash bond purchases in October and pivot towards buying more foreign debt. On Monday, they cut purchase ranges for several maturities and said they might stop buying of debt of more than 25 years. This, along with the poor auction last night, caused long-term yield to jump in Japan…and for the yield curve to steepen. This, in turn, has caused yield curves around the globe to steepen as well.

The move in the U.S. curve this morning is not a major one, but this development further indicates how central bank policies around the globe are shifting towards the goal of steepening their yield curves. If this is indeed the case, our more constructive stance on bank stocks should work very well. We went from negative to neutral recently, but the odds are now rising that we’ll turn to an all-out bullish stance sooner than we had been thinking.

We will continue to keep a close eye on the top-end of the sideways ranges in the KBE & KRE bank ETFs…as well as the 1.9% level on the U.S. 10yr yield. However, we’ll be watching the yield curve closely as well. A move above 10 basis points on the 2yr/10yr spread would give it a nice “higher-low/higher-high” sequence. We’ll also be watching the 3-month/10-year spread very closely. It is now breaking above its 1-year trend-line. If it can steepen further…and move into positive territory (which would also give it a key “higher-high”), it would lead us to turn outright bullish on the banks sooner than we had been thinking (just last week).

Earnings season should provide further headwinds, but group rotation should still provide opportunities.

As we move towards earnings season, we believe it’s going to be tough for the broad stock market to break out in a major way…for the simple reason that we belief the earnings picture will continue to disappoint pictures. However, this does not mean investors cannot make money. If we get the kind of move towards the energy stocks we’re expecting and if the banks stocks can get the help they need from the bond market, these two groups could/should have a BIG impact on investment performance during the last quarter of the year.

Matthew J. Maley

Managing Director

Chief Market Strategist

Miller Tabak + Co., LLC

Founder The Maley Report

TheMaleyReport.com

275 Grove St. Suite 2-400

Newton, MA 02466

617-663-5381

Although the information contained in this report (not including disclosures contained herein) has been obtained from sources we believe to be reliable, the accuracy and completeness of such information and the opinions expressed herein cannot be guaranteed. This report is for informational purposes only and under no circumstances is it to be construed as an offer to sell, or a solicitation to buy, any security. Any recommendation contained in this report may not be appropriate for all investors. Trading options is not suitable for all investors and may involve risk of loss. Additional information is available upon request or by contacting us at Miller Tabak + Co., LLC, 200 Park Ave. Suite 1700, New York, NY 10166.

Recent free content from Matt Maley

-

THE WEEKLY TOP 10

— 10/23/22

THE WEEKLY TOP 10

— 10/23/22

-

Morning Comment: Can the Treasury market actually give the stock market some relief soon?

— 10/21/22

-

What Do 2022 and 1987 Have in Common?

— 10/19/22

-

Morning Comment: Which is it? Is stimulus bullish or bearish for the stock market?

— 10/17/22

-

Morning Comment: Peak Inflation is Becoming a Process Instead of a Turning Point

— 10/13/22