Morning Comment: At Some Point, Stocks Will React To Rising Yields

We’re going to be quick and to the point this morning…….The S&P 500 Index reached a new all-time high yesterday, so the stock market rally off the early October lows continues to be a strong one. However, the internals have not been particularly good this week…as the breadth (which was flat yesterday) and volume (which remains low) have not been very compelling. This is not a big deal (at least not yet). The S&P has rallied seven days in a row…and so these weaker “internals” might only be telling us that the market needs to see a very-short-term breather before it moves higher.

However, there is no guarantee that the market will rally further after it takes a breather. The reason we say this is because long-term interest rates continue to rise. The yield on the 10yr note is now within a whisker of 1.7%...and quite close to its 1.75% highs from last spring. We’d also note that it has broken WELL ABOVE its trend-line from 2018 and made a clear “higher-low.” Therefore, if/when it breaks above those spring highs, it will follow that key “higher-low” with an important “higher-high”…which will remove any questions about the fact that the trend for long-term interest rates is to the upside. (First chart below.)

At some point, this has got to create some headwinds for the stock market. It will also likely cause some underperformance for the tech group…just like it did from September 2020 to March of this year…when yields were also rising at a steady pace (just like they are right now).

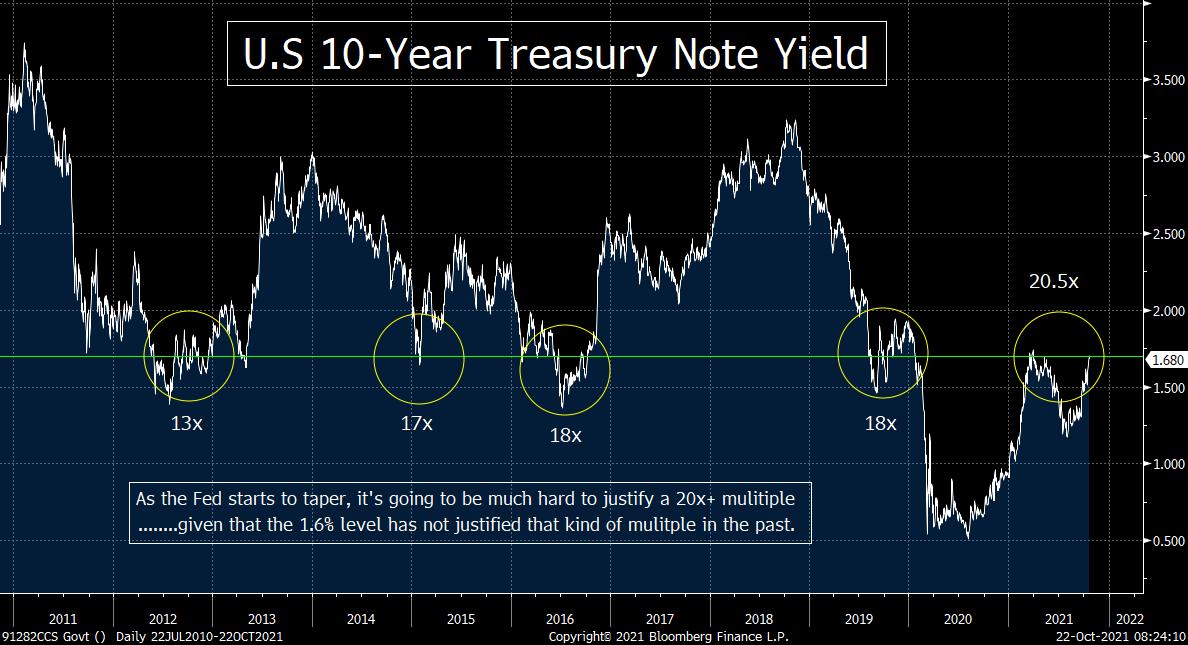

We do NOT agree at all with those who say that today’s interest rates are still low enough to justify today’s level in the stock market. The S&P 500 is trading at 20.5x 2022 earnings and history tells us that a 1.6% yield is not low enough to justify this multiple. As the second chart below shows, the last four times the 10yr yield stood at 1.6%, the multiple on the stock market was 13x, 17x, 18x, and 18x…….In order for the S&P to be trading at the highest level of those examples (18x), it would have to fall below 4,000.

Again, the stock market acts very, very well. However, history tells us that rising long-term interest rates pretty much always create problems for the stock market eventually. Therefore, investors will want to remain nimble as we move towards the end of 2021 and into early 2020.

Matthew J. Maley

Chief Market Strategist

Miller Tabak + Co., LLC

Founder, The Maley Report

TheMaleyReport.com

275 Grove St. Suite 2-400

Newton, MA 02466

617-663-5381

Although the information contained in this report (not including disclosures contained herein) has been obtained from sources we believe to be reliable, the accuracy and completeness of such information and the opinions expressed herein cannot be guaranteed. This report is for informational purposes only and under no circumstances is it to be construed as an offer to sell, or a solicitation to buy, any security. Any recommendation contained in this report may not be appropriate for all investors. Trading options is not suitable for all investors and may involve risk of loss. Additional information is available upon request or by contacting us at Miller Tabak + Co., LLC, 200 Park Ave. Suite 1700, New York, NY 10166.

Recent free content from Matt Maley

-

THE WEEKLY TOP 10

— 10/23/22

THE WEEKLY TOP 10

— 10/23/22

-

Morning Comment: Can the Treasury market actually give the stock market some relief soon?

— 10/21/22

-

What Do 2022 and 1987 Have in Common?

— 10/19/22

-

Morning Comment: Which is it? Is stimulus bullish or bearish for the stock market?

— 10/17/22

-

Morning Comment: Peak Inflation is Becoming a Process Instead of a Turning Point

— 10/13/22

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464