Morning Comment: Waiting For Godot (and Chairman Powell)

Waiting for Powell (and then earnings)

The activity in the stock market was obviously very low on the Wednesday and Friday surrounding the 4th of July…and it’s a good bet that things will remain that way over the next few trading days. First of all, we’re about to begin earnings season, but more importantly, Fed Chairman Powell gives his semi-annual testimony to Congress beginning on Wednesday. This testimony will be even more important than usual after Friday’s much stronger-than-expected employment report. So we expect that investors will be sitting on their hands over the next couple of days.

The strong employment picture raises questions about how aggressive the Fed will be in their upcoming easing program. The strong NFP data took a 50 basis point cut off the table…and raised serious questions about whether we’ll get the three cuts this year that the consensus had been expecting before Friday. It even brought into question whether the Fed will cut at all at their July meeting at the very end of the month.

The Fed has been in the habit for years now of telegraphing their moves on interest rates well in advance…so that expectations can be correctly established long before they make those moves. Therefore, Mr. Powell is going to have to let the market know immediately if a July rate cut is no longer a lock.

Again, the consensus believes that a July cut is still in the cards, but there are definitely some questions about just how aggressive they’ll be with future cuts. So no matter what Chairman Powell indicates about their July meeting, his comments about the rest of the year are going to be critical for investors. This is particularly true since rate cuts from the Fed usually do not help the markets rally immediately. In fact, more often than not, the initial cut is usually followed by a decline in the stock market. So if the Fed tells us that they’re not going to be very aggressive, it could/should have an impact on the broad market. (That kind of development would shift investors’ focus very quickly to the upcoming earnings season…especially the guidance companies provide for the rest of the year.)

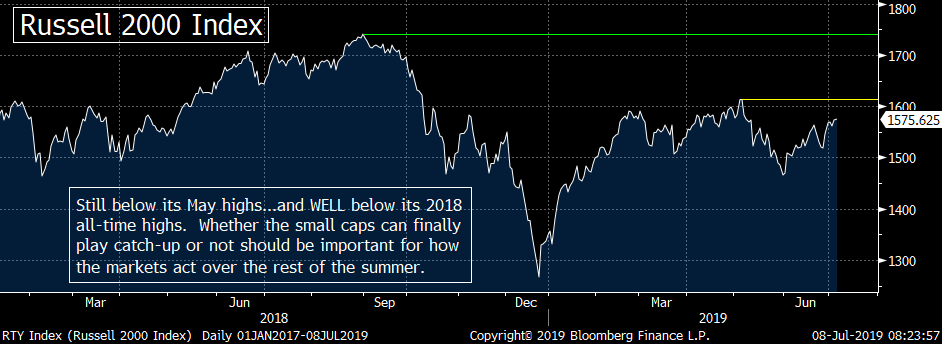

Can the small-caps finally play catch up?

It will be

There are a lot of “ifs” in that last scenario, but with the S&P trying to

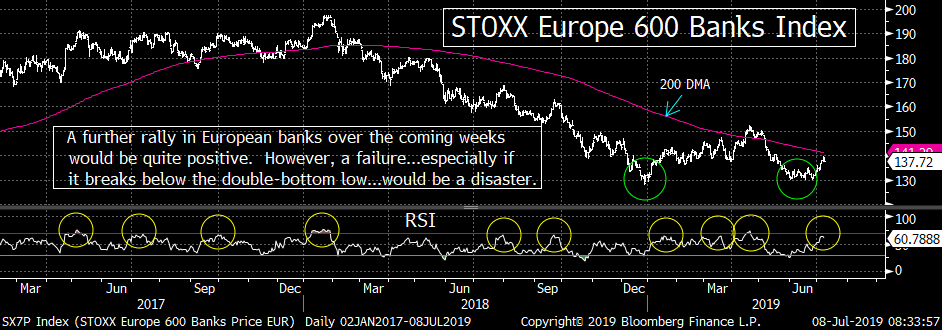

European banks at a key technical juncture

As for today, despite the fact that it should be a quiet day in terms of trading, there will be a lot of talk about Deutsche Bank…their deep cuts…and their decision to get out of the equity business. However, we’d like to focus on the recent action in the stock…and more importantly, on the action of the European bank stocks. DB has rallied almost 20% since June 3rd…and the broad European bank stock index has rallied 5.5% over just the past seven trading days. However, they have both become some-what over-bought and are trading a bit lower in European trading this morning.

The reason we highlight this action (instead of focusing on the impact of DB’s decision will have on the industry) is

Matthew J. Maley

Managing Director

Chief Market Strategist

Miller Tabak + Co., LLC

Founder & CEO; BTFNow.com

275 Grove St. Suite 2-400

Newton, MA 02466

617-663-5381

Although the information contained in this report (not including disclosures contained herein) has been obtained from sources we believe to be reliable, the accuracy and completeness of such information and the opinions expressed herein cannot be guaranteed. This report is for informational purposes only and under no circumstances is it to be construed as an offer to sell, or a solicitation to buy, any security. Any recommendation contained in this report may not be appropriate for all investors. Trading options is not suitable for all investors and may involve risk of loss. Additional information is available upon request or by contacting us at Miller Tabak + Co., LLC, 200 Park Ave. Suite 1700, New York, NY 10166.

Recent free content from Matt Maley

-

THE WEEKLY TOP 10

— 10/23/22

THE WEEKLY TOP 10

— 10/23/22

-

Morning Comment: Can the Treasury market actually give the stock market some relief soon?

— 10/21/22

-

What Do 2022 and 1987 Have in Common?

— 10/19/22

-

Morning Comment: Which is it? Is stimulus bullish or bearish for the stock market?

— 10/17/22

-

Morning Comment: Peak Inflation is Becoming a Process Instead of a Turning Point

— 10/13/22

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464