Looking for Long-Term Value? Look South! (SO)

The following article is sponsored by the Dr. Stoxx Options Letter.

It's hard to believe, I know, but the strongest sector among U.S. stocks last year was the utilities sector. Normally thought of a safe haven for long-term conservative investors, utility stocks were suddenly the go-to place for a very different kind of financial animal: the "momentum stock" trader...at least for a while.

We've seen a substantial correction in the utilities sector so far this year, however, with many of the key players trading off 10% or more from their year-to-date highs. To blame, primarily, is the strong rebound in treasury bond interest rates, which itself has been caused by the end of the Fed's quantitative easing program (among other things). As rates climb, those looking for income and safety tend to pull money out of stocks and plow into safe havens like bonds and treasuries. This is why a chart of the 10-year yield with the utility stock index overlaid shows a clear tendency of the two asset classes to mirror each other:

[source: MarketWatch]

I'm in the camp that counts this pullback in utilities as a great buying opportunity. Nothing has changed in the fundamentals of the underlying companies; and the lower share price makes their dividends all the more attractive. Right now you'll pay less for more yield than any time since October last year. Among domestic utilities, there are 5 big players: NextEra Energy ($46B), Dominion Resources ($42B), Southern Company ($42B), American Electric ($28B), and PG&E ($26B). All 5 companies are trading at least -10% below their 52-week highs. And all 5 companies have seen their dividend rates climb at least 50 basis points, making them attractive places to park cash for those looking for discounted income.

My favorite among the big 5 is Southern Company (NYSE: SO). This utility company generates electricity through coal, nuclear, oil, gas, and hydro and distributes it in the states of Alabama, Georgia, Florida and Mississippi. Since peaking at $53.16 in late January as investors sought the relative safety of utilities, the stock has fallen about 14% in less than three weeks' time, the largest pullback of the top 5. That is a move statistical importance: it hasn't been matched since the tail-end of the Great Recession, a time with a very different economic context. Shares are therefore ripe for a bounce from here.

As of February 17th, the dividend yield of SO is 4.58%, the largest yield of the top 5, and about 110 basis points above the large-cap utilities index average. At the last earnings announcement on February 4th, the company came in a bit light on eps, missing its 4th quarter estimates. This was largely due to charges related to delays in the building of a $8 billion nuclear plant in Georgia, along with a drop in residential sales. The good news, however, is that industrial sales were up 3.3% quarter on quarter, much higher than industry average. This bodes well going forward as industry in the region served by Southern is an a strong upswing.

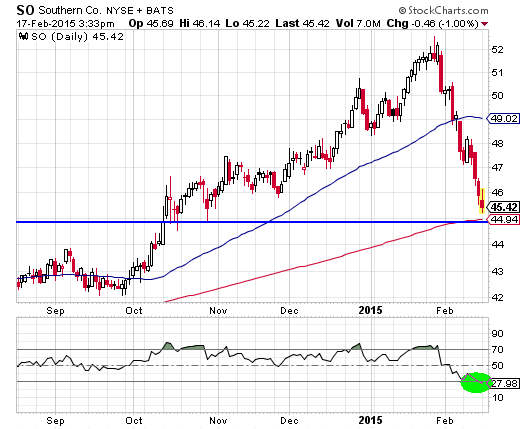

As the chart below shows, SO is in a deeply oversold condition. Shares have already completed a 61.8% Fibonacci retrenchment of its August to January run. They are also touching its 200-day moving average which coincides with an area of former price support. The Relative Strength Index (RSI - 14) is printing a rare oversold reading below 30.

All the above combine to make Southern Company a compelling buy for long-term investors, especially those looking for income. I consider shares to be attractive at this level, and I expect a rebound toward the 50-day moving average (currently: $49) over the next few weeks.

If you buy the shares, you can collect the 4.6% dividend after 12 months. But in the Dr. Stoxx Options Letter, we have a way of collecting even more than that in half the time. Our put-write strategy allows us to collect a 5.5% dividend in 6 months, which annualizes to a 11% yield. This is a low-risk way of adding income to our trading capital, and if we are put the shares, we can always sell calls against the shares to lower our cost basis even further.

Recent free content from Dr. Thomas Carr

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464